The Power Law is a mainstay in Venture Capital, which means that a small percentage of investments is responsible for a large percentage of overall return value. This shouldn’t come as a surprise as we have all read the headlines of outliers having big IPOs or acquisitions.

A great set of research was published (found here) by Sapphire Partners, one of the more active Limited Partners that has invested in a large number of prominent VC funds. One of the questions they focus on is a very relevant question we ask ourselves, “Do your odds of making better returns improve if you only invest in either enterprise or consumer companies?”

The key takeaways:

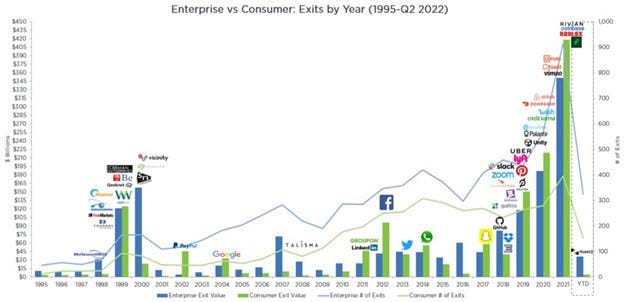

Portfolio value creation in enterprise tech is often driven by a cohort of exits, while value creation in consumer tech is generally driven by large, individual exits.

Billion-dollar enterprise exits can occur in both up and down markets as enterprise companies’ consistency of outperformance comes from both IPOs and large M&A to PE and corporations (hat tip Figma).

Enterprises exit power law is one of persistence and resilience.

The Indelible Viewpoint

The value proposition for investing in enterprise technologies can be broken down into a set of categories

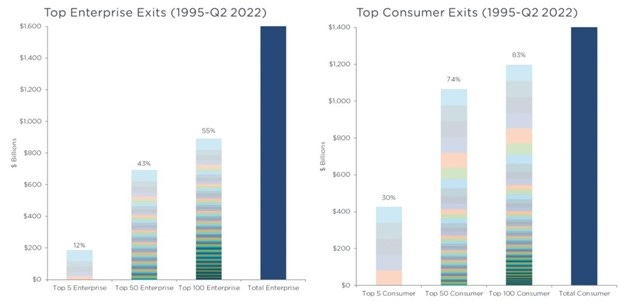

Power Law Cluster - The data indicates there is a tendency towards a “one hit wonder” return profile within consumer segment. However, the clustering of enterprise winners indicates an important difference in the probability profile of achieving outlier returns. It is because of this return distribution that the portfolio management of a VC investor is important. To create a high performing Fund, the Enterprise investor must be able to create a basket of successful exits.

In a Consumer fund, the VC would need to avoid “missing out” and therefore would more likely need to employ a “spray and pray” approach as the probability of the outlier that drives returns is lower.

In an Enterprise Fund, the VC can manage a better balance between concentration and diversification without the fear of “missing out”. The high value-add approach of assisting in the build and scaling of Enterprise will increase the likelihood of creating the cluster of successful exits that is necessary.

Global Market - Many country markets lack the population size to be a single destination market to create sufficient scale for Venture returns. Global expansion is a necessity for many. There are numerous examples of small population markets achieving this expansion. Within ASEAN, the default expectation is that Singapore (5.7M people) startups are global or at minimum regional. We also see similar international expansion from Australia (25.7M people) where companies like Canva, Atlassian, GO1, SafetyCulture, and several others have achieved scale growth and unicorn status. Similar stories are echoed in Latin America and regions of Europe like Scandinavia and the Baltics.

There are enabling characteristics that a market should possess in order to be a launching pad in order to increase the probability of success to enter new markets. I refer to these as the Gateway Factors.

Malaysia as a Gateway - Gateway Factors revolve around a general theme of describing the similarities of the markets and relevance of the gateway to act as a starting point. The full depth is a topic for another essay, but we look at our home market in Malaysia as possessing many of the requisite factors that would serve as a key gateway market.

For enterprise, Malaysia is home to thousands of multinational corporations (MNCs) which immediately brings a global perspective and understanding of the business dynamics of global enterprises. This is critical to be capable of building startups that can service global markets. Within the business community, there is a diversity of each size of enterprise to provide a substantial testing ground to reach product market fit before scaling. Malaysia is also a multi-lingual, multi-cultural society which provides a simulation for a startup to experience prior to expanding internationally. These encompass just a few of the Gateway Factors that make Malaysia a destination for building and scaling a Enterprise tech startup.

Pandemic Tech Adoption – Historically, building an enterprise SaaS business meant having a core focus on the US market. While this remains a large and attractive market, the rest of the world, Southeast Asia included, has sped up the pace of their tech adoption. The forced lockdowns pushed companies to adapt to a work from home environment and then transition to some form of hybrid. In doing so, many realized the value of implementing technology and have overcome the biggest hurdle, which is the first step. There is an inertia behind adoption that will continue to build.

When we look at the way companies interacted with customers, the pandemic had forced an adoption acceleration. In the APAC region, this is estimated at a 4-year acceleration along the trendline. While, the post-pandemic period is still nascent, even a reversion would be unlikely to offset the full gains and the trendline will continue.

Beyond customer interactions, we have seen a dramatic shift in the digitization of offerings. Globally, this represents a 7-year acceleration. In APAC, we have led the shift with over 10 years’ worth of acceleration in tech adoption. This acceleration is a boon for digital businesses.

Exit Opportunities – Pathways for exit are critical in order to realize the gains from a VC investment. Within consumer segment, the most probable pathway to exit for a consumer product is via IPO. Considering the down IPO market that we are currently facing and the pessimism in the market for the foreseeable future, this will likely make it challenging for consumer plays. This is opposed to the broader options of Enterprise.

Enterprise products have had an active M&A market which is most recently represented by Adobe’s $20B acquisition of Figma. There are many other examples as it is fertile ground within the Enterprise segment. There is also a viable IPO market. So, net-net, there are ample possibilities to generate exit opportunities within an Enterprise focused portfolio, certainly sufficient to generate the clusters needed for the Power Law.

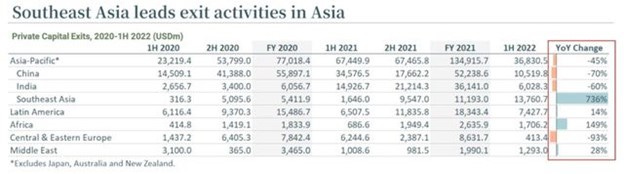

According to Global Private Capital Association (GPCA) data analyzed by DealStreet Asia, Southeast Asia has presented a bright spot for exit with 1H 2022 exceeding the full FY 2021 value. As Southeast Asia continues to mature as a startup ecosystem, the outlook for exit opportunities is favorable.

Indelible in Action

It is the view of this author that the above characteristics should drive the portfolio and investment strategy of a VC. We have seen firsthand the success of companies created in Southeast Asia becoming global products. A few examples include:

RunCloud, a cloud control panel, which counts only 8% of its revenue from its home country. This company continues to grow and attract interest from international investors.

VOX, a ready-to-use A.I. assistant platform to automate conversations and sales conversions, has seen significant traction from major brands and has even won pitch competitions in Silicon Valley.

Vase.ai, a consumer insights platform, has seen substantial traction and greater product demand from external markets.

If you’re interested in learning more about what Indelible Ventures is doing or where we see opportunity, please reach out directly.