It is unlikely that anyone has not seen major headlines regarding Venture Capital that have been regularly gracing news publications and social media feeds. It can become a bit difficult to sort through which are simply click-bait and which actually are providing insight.

There are a few points that have prompted me to want to segment the hype from the reality.

A recent Forbes article was published titled “Emerging VCs Struggle To Raise Funds As Nervous Investors Park Their Money In Big-Name Firms”.

According to Pitchbook, U.S. venture capital firms alone have raised a record $150.9 billion through the end of September 2022 from their investors. A Sifted article puts European VC at $16 billion. An article from Nikkei in mid-2022 put Asia at $3.1 billion which nearly matched full 2021.

So, while on the one hand the reporting is signaling record fundraising, there are other reporting that discuss the difficult environment. So, let’s separate a little by of Hype from Reality.

Funds Committed to Venture Capital

Hype: Although valuations have gone down, capital commitments continue to rise. This has led many to claim that a bubble is still inflating.

Reality: Venture Capital is seeing a broader range of investors allocating capital into the space while the existing institutional investors are increasing their portfolio allocations. However, broad swathes of private companies remain untapped by Venture Capital.

It is certainly true that huge amounts of capital have been allocated to Venture Capital. This is without question. It is also true that we have seen large valuation cuts in the public markets and late stage private companies. The need for a correction in asset prices is clear. However, the disconnect is centered on the fact that asset prices are correcting while more capital still is being allocated.

To understand the reality, we must view certain contributing factors that provide clarity to why the increasing capital in VC is happening:

New Entrants – Among the investors that contribute capital into VC Funds, this has historically been institutional investors. However, the field is broadening as more categories of investors start moving more heavily into the space. This is largely due to the long time horizon and the appeal of outsized returns, even excluding the bubble in valuations of the last couple years.

Sovereign wealth funds (SWFs) have accounted for large allocations to boost mega funds such as Softbank. These same SWFs are key contributors to other large VC firms moving significantly greater amounts of capital.

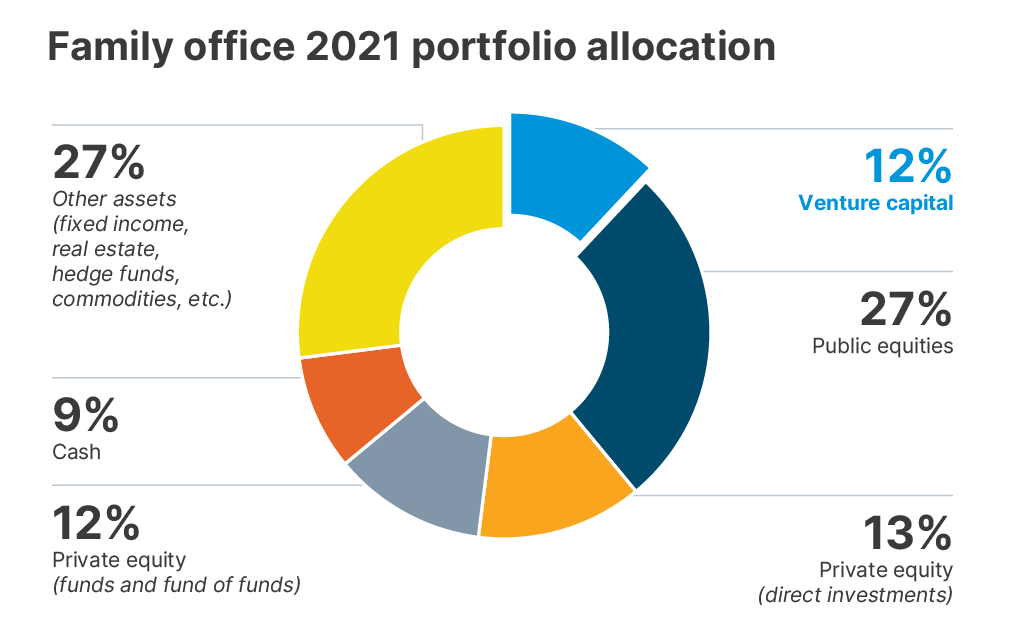

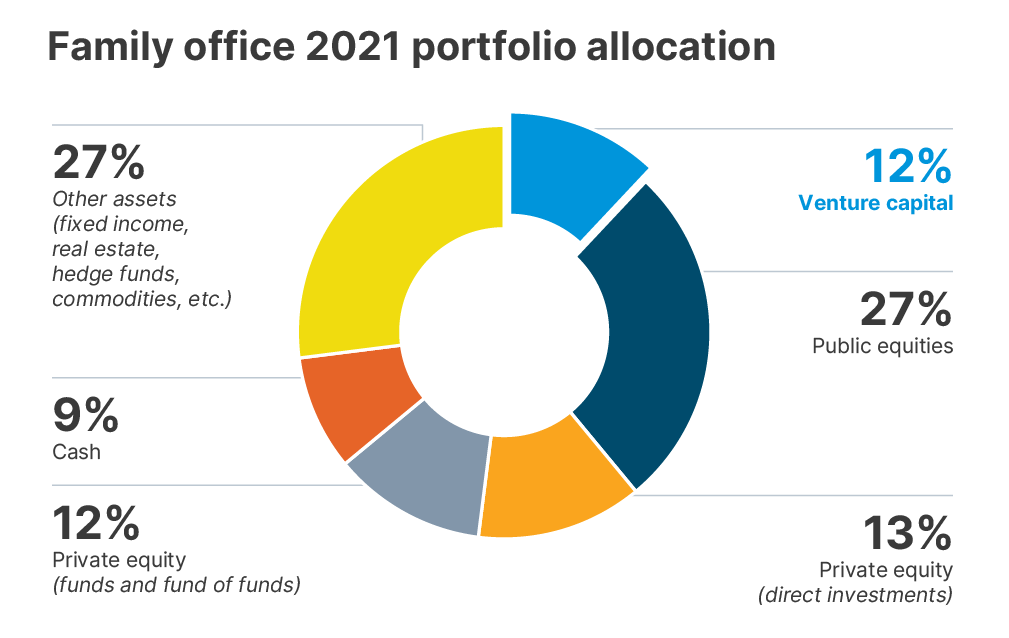

Family Offices have been increasingly entering into the Venture Capital space. This has opened an extremely large pool of capital that was previously on the sidelines. A few family offices had made entrances into the space, but this has been increasing.

High net worth individuals have also been lured into Venture Capital. These are accredited investors that may have significant wealth but not necessarily a family office managing it.

The sum impact of new entrants becoming more interested and dedicating more capital is driving up the allocations that Venture Capital receives. Many of these new entrants, like Family Offices and HNWIs are attracted to the opportunities that Emerging Managers present as the first access point into the space.

Portfolio Allocations – Investors both new and existing within the VC ecosystem have been ratcheting up their allocations to the space. These allocations range from 5% to 20% on average. Organizations such as Cambridge Associates have been advocating to allocate 40% or more to private assets, with a 20% allocation to VC. This has been represented by the allocation data they have compiled which illustrates the widening gap for the top decile.

Slowing the Herd – Investments in VC-backed companies have become inflated, but the greatest of these exaggerations have come from the later stages, which are highly correlated to public market valuations. With the easy money, the public markets saw an incredible bull market that saw the implied valuation multiples expand well beyond historical averages. With the run up in the public markets, later stage private market investors felt more confident to pump up valuations with the promise of a buoyant IPO market. This then trickled down through the private markets into the earlier stages with lessening and lessening impact on the premium.

The excesses led to herd behavior that is not unique to VC, but has occurred across every bull market in every asset class whether public markets, real estate, or VC. It is when the music stops that the exuberance gets reigned in. The public markets have corrected, and the same trickle-down impact has occurred.

VC investors with experience realize that they are investing across multiple cycles as these are long term. Corrections in the later stages are to be expected, but it is during these times when opportunities are created.

Untapped Markets – The greater participation of HNWIs and family offices is a differentiated set of networks. These investors are getting tapped by Emerging Managers that also have diversified networks of startups. Across the globe, there are incredible founders starting meaningful companies. Many markets remain untapped and much of the capital that is being raised is waking up to that fact.

Looking across the VC landscape, startup ecosystems have grown and matured across the globe. In the US, it is no longer Silicon Valley but there is New York, Los Angeles, Austin, Miami, and on and on. The Cambrian explosion of startups has occurred in Latin America, Europe, Africa, the Middle East, South Asia, East Asia, and Southeast Asia. Many of these are still developing and the availability of the opportunities still far outstrips the mountain of capital that has been raised within VC.

Emerging VCs Struggle

Hype: Emerging Managers (VC managers on Fund 1) are struggling because Institutional Investors are putting their money with established VCs.

Reality: The reality is that Institutions rarely, if ever, invested capital with Emerging Managers. This has never stopped emerging fund managers before and it is not stopping them now.

Reading this Forbes article, it is an unfortunate collection of quotes and points that have some level of relevance in the VC space. Unfortunately, there is little to no relevance to the title argument. Through the article, there are two primary assertions that are used to frame a struggle:

Claim: Institutions are deciding to invest in established firms.

This is not wholly inaccurate and the quote used is correct: “no one gets fired for investing in Coca-Cola stock,” says Garth Timoll, managing director at Top Tier Capital Partners. However, institutional investors rarely if ever invest in first time fund managers so the dependency on this “Coca-Cola” decision is not relevant to them. This is simply misplaced directionally.

There is an impact of this decision matrix, but the article inaccurate illustrates it. What we see in the market is a consolidation of VC firms around unique value propositions that are offered to the Limited Partners. Many firms in the space are targeting a Scale business model. Examples would be Sequoia, A16Z, Insight, and several others. These are the players that are launching “mega funds” into the market to accomplish a Scale objective. It is these progressively larger Funds that are creating the demand on the institutional allocators to decide whether to allocate to their “Coca-Cola” brand Fund or some other Fund.

The reality for Emerging Managers is that their commitments are generally coming from high-net-worth individuals (HNWIs) and Family Offices. It is not that they wouldn’t want the larger check sizes that come from institutions, but most institutions as a policy do not invest in 1st time Funds. This is the reality. Fortunately for Emerging Managers, HNWIs and Family Offices are adding allocations to Venture Capital at a faster pace than ever before and advisors to them are suggesting increasing their allocations.

It is clear why allocations to emerging managers are increasing as well. The data consistently shows emerging managers being disproportionately being represented in the top tier of fund manager performance.

So, if anything, the struggle that Emerging Managers have is not related to the decisions of institutional investors. It is related to finding and connecting with HNWIs and Family Offices who, by nature, are less visible and more difficult to know the “who, where, when” of connecting. That said, as data from VC Lab shows, commitments to emerging managers continue to accelerate.

Claim: Investors in VC Funds are reneging on commitments.

There is anecdotal evidence that this has happened, however, it is uncommon. When the economy struggles, an individual or a family office may see priorities shift or even struggle with the liquidity to keep certain commitments. These scenarios could potentially happen, but they are rare. It is important that investors, whether individual or family office, be aware of portfolio allocation strategies to ensure they are not overcommitting and they do (with rare exception), otherwise they wouldn’t have accumulated their wealth in the first place.

Don’t let the headlines deceive. There is a correction that is impacting the top of the market, but Emerging Managers are thriving and will be the driving force to open new geographies and prove out differentiated investment theses that advance the industry overall.